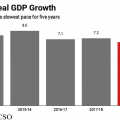

National and international agencies, including the Reserve Bank of India (RBI), the International Monetary Fund (IMF), and the World Bank, in the last few months, have been steadily downgrading their FY 2020 growth forecasts for India. The most pessimistic growth rate of all forecasts is from the international rating agency Moody’s at 5.8%.

Table 1 FY 2020: India's Likely Growth Rate (%): Various Forecasts

Agencies Previous Latest

ADB 7.2 6.5

IMF 7.0 6.1

Moody's 6.2 5.8

OECD 7.2 5.9

RBI 6.9 6.1

World Bank 7.5 6.0

The reasons, widely agreed on, are fall in domestic demand (comprising domestic consumption and investment) and external demand and investment. Fall in domestic demand well noted in a range of manufactured goods right from auto sales to biscuits and tooth paste consumption in rural areas. Sale of passenger vehicles in the second quarter of 2019 declined by close to 30%. The sale of commercial vehicles also had a rising negative rate of growth (-28%) in the second quarter of FY 2020 as compared to -10% in the first quarter. Vehicle registrations (which include 2 and 3 wheelers and passenger vehicles) - despite the festival season discounts - have fallen by 12.9%. The biggest fall is in the category of passenger vehicles which is by 20%.

Domestic consumption

The Nielsen consumer survey results painted a bad picture of falling consumer demand. The rural households are continuing a falling trend in consumption of fast moving consumer goods, led by salty snacks, biscuits, spices, soaps, and packaged tea along with non-food items. Rural consumption is shrinking by 10% for the third consecutive quarter beginning from the third quarter of the last fiscal.

External demand for Indian goods (which is reflected in the export statistics) has also been falling. India’s exports comprising of petroleum, engineering and leather products, chemicals, and gems and jewellery decreased by 6.6% to reach $26 billion in September 2019. Imports fell by a much larger percentage, reducing the trade deficit to the lowest at $10.9 billion in seven months and as compared to the 2018 September figure of trade deficit which was $14.95 billion. Reasons attributed are slump in global demand and trade tensions. The World Trade Organization has already cut the world trade growth rates for 2019 and 2020 to 1.2 % and 2.7%, respectively.

In normal times, trade deficits are not a concern with comfortable levels of foreign reserves; and rising imports against a steady export volume level would not be a bother. But falling imports of capital and intermediate goods accompanied by declining industrial production are not good signs for India. In the present context, the current slowdown with only 5.5% growth in the first quarter (April-June 2019) and the industrial production index growth in the negative territory (-1.1%) are ominous signs for the economy. The contraction of industrial production in India’s factory output also contracted in August 2019, for the first time in seven years.

Though the critics would like to place the blame on the November 2016 demonetisation and the introduction of Goods and Services Tax (GST) which came into effect from July 2017, one has to look at the Table 2.

Table 2: India's Quarterly Growth Rates (%): FY 2015-FY 2020 (Q1)

Fiscal Year Q 1 Q 2 Q 3 Q 4

2015 8.0 8.7 5.9 7.1

2016 7.6 8.0 7.2 9.1

2017 9.4 8.9 7.5 7.0

2018 6.0 6.8 7.7 8.1

2019 8.0 7.0 6.6 5.8

2015-FY 2020 (Q1)

The sudden disruption in economic activities caused by cash crunch, especially in the rural parts of the country resulted in a severe jolt and the growth halted. This was most severe in Q3 of FY 2017 (2016-17) and the adverse effects of inadequate liquidity lasted until Q3 of 2018. It was followed by a slight recovery, which did not last long, as the world conditions altered. The foreign portfolio investors began to pull their funds out of India as India was no longer perceived to be an attractive place for investment. Causes this time were several —mounting non-performing assets (NPAs); fear of bank failures and scams; detected frauds and the resultant uncertainties, all leading to evaporation of confidence in the Indian economy. Further, inefficiencies in enforcement agencies and alleged corruption, resulting in the detected culprits going scot-free do not promote better governance.

Raise confidence

Table 3 reflects the poor confidence in the economy. India which was ranked on an overall basis at 58 among the 141 countries by World Economic Forum last year has lost 10 places in the latest ranking. It is now ranked at the sixty eighth position. One can derive some comfort that it is not below 70, which is right about the half of the 141 countries. The best rank among the 12 parameters is 3 and the market size is the relevant parameter, which is determined by sheer size of the population. That is not a surprise at all.

The surprising thing is India’s rank in Information and communications technology (ICT) adoption is 120, among 141 countries. India boasts of ICT superiority, with services exports being dominated by ICT related services. It is obvious that the so called ‘Fourth Industrial Revolution’ based on an explosion of communication and technology has not yet touched the country. Spread of ICT is facilitated by uninterrupted supply of electricity in rural areas and with agricultural produce being swiftly transported by infrastructural facilities. The rank in infrastructure shows India to be at the seventieth position. The ranking in regard to institutions, another parameter is equally uninspiring.

Table 3. India's Rank in World Competitiveness among 141 Countries

Parameters Rank

1. Market Size 3

2. Macro Economic Stability 43

3. Financial System 40

4. Infrastructure 70

5. Health 110

6. Business Dynamism 69

7. Institutions 59

8. Labour market 103

9. Innovation Capability 35

10. Skills 107

11. Product Market 101

12. ICT Adoption 120

The low ranks in key areas and the overall rank partially explain why the manufacturing units in China, which are now seeking relocation outside China due to trade war between the two super economic powers, are preferring countries in the ASEAN region. Vietnam which was previously ranked lower than India, gained 10 places as against India’s loss by 10 places. It has attracted many factories located earlier in China. It is now ranked at the sixty seventh position, one place higher than India.

All ASEAN countries have higher overall ranks as compared to India (Indonesia at the fifth position, Malaysia is at the 27th position, Philippines is at the 64th position and Thailand is at the 40th position). The high and middle end manufacturing companies are shifting to Singapore and

Malaysia and Thailand, the lower end units are shifting to Vietnam and Indonesia.

Long time lags

The implementation of structural reforms takes time, generally three to five years. The resolution of the NPA issue, which began in earnest last year, is now facing legal hurdles under the Insolvency and Bankruptcy Code. The banks have to take big haircuts when forced to put NPSAs on sale for raising resources or wait for a longer time. The RBI has been cutting the policy rate since the economy needed booster doses for stimulating consumption and aggregate demand (five times this year, totaling in all by 135 basis points). It is now 5.15%. There is no visible improvement in domestic consumption and investment. Another cut in the repo rate in December is indicated.

Monetary policy changes do not give immediate results. In the meanwhile, just a fortnight ago, the Bloomberg economists have sounded the alarm about another recession, as their global growth tracker slowed to 2.2% in the third quarter of the calendar year 2019 from 4.7% at the start of 2018. Global growth is forecast at 3% for 2019, its lowest level since 2008–09 and a 0.3 percentage point downgrade from the April 2019 World Economic Outlook. The new chief of IMF has also recently warned the world of a serious risk of a new recession.

Need for dynamic response

India need not worry about the IMF and its usual ‘Washington Consensus’ and the ‘one size fits for all’ remedy of fiscal discipline. India should loosen its fiscal policy. Tax incentives for investment such as reduction in corporate tax rates and surcharge roll-back of contentious surcharge on FPI have yet to work through. So, what we need is a direct assault. India’s fiscal target which is 3.3% is not sacrosanct now. Any slippage would be appropriate.

The government should increase public spending on infrastructure projects. Incomplete projects should be completed. That will send out a strong signal. Public debt is at a sustainable level. The latest statistics reveal it was 125% (public debt 70 % and private debt 55 %) of GDP as against China’s 247% of GDP. External debt is also small at 20% of GDP. Foreign reserves stand at around $429 billion, with the highest ever foreign exchange assets component at around $397 billion, gold reserves at around $27 billion, Special Drawing Rights (SDRs) with the IMF, and others at around $5 billion.

-

The author is a Research Professor, ICP Programme, University of Tunku Abdul Rahman, Kampar, Perak, Malaysia; and Visiting Adjunct Professor, Amrita School of Business Bengaluru Campus.

[The views expressed by the author in this article is his own.]

Add new comment